With many inroads conquered, growth in U.S. plastic container demand to slow

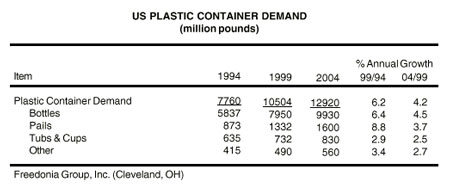

Still, the growth rate of U.S. plastic container demand is expected to increase by more than 4% yearly, bringing total demand to nearly 13 billion pounds in 2004, amounting to a total of 130 billion units. However, the 4.2% annual growth rate of U.S. plastic container demand from 1999-2004 is down from that of 6.2% from 1994-1999 (see chart).

In addition, container value will advance more than 5% annually during the 1999-2004 time period to $13 billion. These projections are among the trends presented in Plastic Containers, a new study from The Freedonia Group Inc., a Cleveland-based industrial market research firm.

Plastic's penetration of traditional glass, paperboard and metal packaging applications will be based on advantages such as clarity, light weight, strength, shatter resistance, good barrier properties and ease of opening and dispensing. The popularity of smaller sized bottles in markets ranging from soft drinks to cosmetics and toiletries will also fuel unit gains.

Bottle boom

Plastic bottles, which already account for 75% of all plastic containers by weight, will log the best growth, at 4.5%. Advances will be propelled by strength in traditional markets such as pharmaceuticals and carbonated soft drinks, as well as by opportunities in novel applications such as beer. Growth will slow from the historical pace, however, as the most accessible inroads have already been achieved.

Plastic pails will also enjoy favorable, although below-average, prospects based on their light weight and performance advantages compared to metal pails.

Even more modest growth is forecast for plastic food containers. Demand for these will increasingly track growth in the mature food industry, as plastics have now largely supplanted competitive paperboard containers in key applications like produce and dairy packaging.

PET, HDPE remain strong

Among plastics, polyethylene terephthalate (PET) will exhibit the fastest growth. PET bottles will continue to supplant aluminum cans in the bedrock soft-drink market, based on PET bottles' clarity, high-barrier properties, availability in multiple sizes, design flexibility, competitive pricing and resealability. Good opportunities are anticipated for larger single-serving beverage and hot-fill food and beverage applications.

While PET will be the fastest-growing plastic container resin, high-density polyethylene (HDPE) will remain the most widely used. HDPE container markets are more mature, with the resin having already supplanted competitive packaging materials in key applications such as motor oil and household cleaners. Good opportunities are expected in areas such as milk and juice bottles, primarily in the smaller sizes.

Other leading plastic container resins include polystyrene (PS), polyvinyl chloride (PVC), polypropylene (PP) and low-density polyethylene (LDPE).

Plastic Containers was published in September and consists of 213 pages. The new report is available for $3,600 from The Freedonia Group.

For more information or to purchase a report: The Freedonia Group Inc., 767 Beta Drive, Cleveland, OH 44143-2326, Tel: 440-684-9600, Fax: 440-646-0484, Email: pr@freedoniagroup.com

Edited by Bill Noone