Impact of Arabian Gulf ethane on the global petrochemical industry

Contents

Ethane Supply

Driving Forces

Crude Price Scenarios

Starting from almost nothing in 1973, production of ethylene-based petrochemicals in the Arabian Gulf has grown so explosively that the region is now the predominant exporter to the world market. This success has been propelled almost exclusively by the recovery of low-cost ethane from natural gas as feedstock for ethylene production.

Trichem recently published a multi-client study, "Impact of Arabian Gulf Ethane on the Global Petrochemical Industry," to analyze the outlook for additional ethane recovery and its utilization as ethylene plant feedstock in seven of the Gulf countries physically endowed with natural gas resources, namely Saudi Arabia, Iran, Kuwait, UAE, Qatar, Bahrain, and Oman.

The future growth in Arabian Gulf ethane-based ethylene production capacity is of crucial importance to the industry since ethylene is the most utilized building block in the petrochemical industry, and ethane cracking—as opposed to naphtha cracking—reduces the co-production of propylene, butadiene and aromatics. The impact on the propylene supply/demand balance of such developments could be of considerable significance to refiners creating greater opportunities in the petrochemical market.

Ethane Supply(Return to Contents)

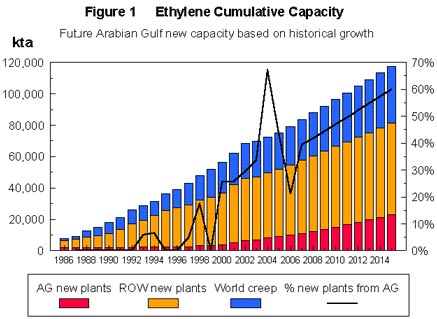

The share of supply of the Arabian Gulf (AG) to the global ethylene demand by 2005 appears relatively modest at around 8%, assuming a 90% operating rate. However, the AG share will have doubled between 1987 and 2005. A better measure of the impact is the annual percentage of new plant capacity contributed by the AG. The bars represent the cumulative capacity of new plants and capacity creep. The solid line represents the additional new plant contribution annually from the AG.

Based on current plants under construction, the AG region's share of the world's new plants will rise from 26% in 2000 to about 40% in 2005. If a new plant in the AG region is added at the same rate as achieved historically, then over the period 2005-2015 about half of the new ethylene plants built globally will be located in the AG, almost all within five of the seven countries studied.

The study examines the main drivers of ethylene plant capacity growth and the constraints on ethane availability and ethylene/derivative plant competitiveness and profitability, which could limit investment in new plants in each of the seven study countries.

Driving Forces(Return to Contents)

The three main driving forces for future investment in ethane recovery and ethylene/ethylene derivative production the Gulf countries are:

Trichem foresees the total crude oil production in the seven study countries rising from around 17 million barrels per day (MMbpd) in 1999 to 24.7 MMbpd in 2010 and 30 MMbpd in 2015. Associated gas production will also increase at approximately the same rate as crude production and there will be major increases in non-associated gas production in Iran and Qatar and, to a lesser extent, in Saudi Arabia, the UAE, Oman and Bahrain. The potential amount of ethane available from these associated and non-associated gas streams is assessed in the study and compared with commitments already made for ethylene plants in operation or under construction.

Ethane recovery costs vary significantly with the concentration of ethane in the gas. Ethane recovery from wet associated gas or from wet non-associated gas prepared for liquefaction to LNG adds little to the normal separation costs of methane from other liquid components provided that such a recovery facility is incorporated in the original separation plant. Retrofitting to permit ethane recovery can be expensive and separation of a dry methane/ethane fuel gas is very expensive.

Hence, in countries with low ethane recovery costs (Saudi Arabia and UAE), ethane is usually priced at its alternative value, i.e., fuel gas. Where recovery costs may be higher (possibly Iran, Qatar and Kuwait) this could be reflected in the price. More particularly, where foreign partners are invited to participate in petrochemical joint venture, the price is usually a commercial negotiation (Kuwait, Qatar and UAE).

Large-scale investment in ethylene production in the Gulf was initially driven by the availability of low priced ethane and was centered for many years in Saudi Arabia. When ethane availability started to become constrained for additional ethylene complexes, the authorities decided to supply propane and A180 condensate (naphtha) at a market price discount to bolster low-cost feedstock supplies. An additional incentive to do so was to widen the product slate to propylene and, to a lesser extent, aromatics as building blocks for their derivatives.

There are at least two downside risks to such a discounting strategy. First, there is the prospect that it could be seen as unfair trading practice because feedstock is being subsidized. Second, it could be much less economic at the current Saudi discount for LPG and naphtha of 30%, if ethane could be made available and the crude oil price is maintained above around $12 per barrel.

The economic uncertainties and risk of trade repercussions are sufficient to conclude that large-scale development of ethylene plants in the Gulf based exclusively on propane and naphtha feedstocks is unlikely.

Crude Price Scenarios(Return to Contents)

The study considers the impact on Gulf ethane of three crude price scenarios for the period 2005-2015:

Although there is some export of ethylene from the Gulf, the profitability of ethane-based ethylene production is obtained from complexes, which convert ethane via ethylene to derivatives that are less costly to ship to the two main target markets, Asia and western Europe. Thus, a valid analysis of Gulf ethylene from ethane competitiveness is to compare the cash cost of delivering a key derivative, such as HDPE (high density polyethylene), from a Gulf petrochemical complex to Asia or western Europe with that of local producers or other HDPE exporting countries.

Such a competitive analysis was made and the results show that:

Trichem estimates that by 2010, the seven Gulf countries will have approximately 21 million tonnes/year (MMtpy) of ethane potentially available for recovery over the period 2000 to 2010 (in addition to the 5.2 MMtpy recovered in 2000). However, it appears reasonable to foresee the recovery and utilization of only half of that ethane.

Five of the seven Gulf study countries are likely to see investment in new ethane-based petrochemical projects by 2010 corresponding to approximately 9.8 MMtpy ethylene capacity. Saudi Arabia is likely to account for half of this new investment, being the best placed in terms of ethane availability and recovery.

Such new capacity will comprise 25% of the 39 MMtpy additional global ethylene capacity expected by 2010, increasing Gulf ethane-based share of global ethylene demand from 5.1% in 2000 to 11% in 2010. Trichem expects ethane cracking in the region to increase at a lower rate than historical growth beyond 2005.

Production of an additional 9.8 MMtpy ethylene from ethane in the Gulf would reduce the supply of approximately 4.5-5.5 MMtpy propylene co-product from potential alternative naphtha-based plants elsewhere. To satisfy the global propylene supply/demand balance, this reduction in supply should encourage higher propylene/ethylene cracking ratios in new naphtha-based plants outside the Gulf and additional investment in increased propylene production from refinery FCC units.

The impact of ethane-based Gulf ethylene on global ethylene and propylene supply could double if current high crude prices were to be sustained over the next decade. Such a scenario is highly unlikely bearing in mind the likely effect on world oil demand growth and the encouragement of alternative non-OPEC supply.

Copies of the full report, "Impact of Arabian Gulf Ethane on the Global Petrochemical Industry" can be obtained from Trichem Consultants Ltd, River Park House, 225 High Road, Wood Green, London N22 8HQ, UK. Tel: (44) 20 8888 4460, Fax: (44) 20 8889 76 99. e-mail: consultants@trichem.co.uk

Edited by Russ Swan, Managing Editor, EuroChemWeb.com

and David Nakamura, Managing Editor, Hydrocarbon Online